Market Structure - Multi-TimeframePivot based channels for 8 individual time-frames. This can be used to identify the support and resistance level for different time-frames. Recommended is 1min as timeframe for the candles sticks. The direction for every pivot-channel is marked in green for bullish and red vor bearish. There exists alerts for Choch and BoS for every timeframe.

Cari dalam skrip untuk "market structure"

Market StructureSimple script to Plot Horizontal Lines at turning points of the market. Often times, these key levels can indicate a potential trade when price breaks above/below.

Smart Money Concepts by WeloTradesThe "Smart Money Concepts by WeloTrades" indicator is designed to offer traders a comprehensive tool that integrates multiple advanced features to aid in market analysis. By combining order blocks, liquidity levels, fair value gaps, trendlines, and market structure analysis, the indicator provides a holistic approach to understanding market dynamics and making informed trading decisions.

Components and Their Integration:

Order Blocks and Breaker Blocks Detection

Functionality: Order blocks represent areas where significant buying or selling occurred, creating potential support or resistance zones. Breaker blocks signal potential reversals.

Integration: By detecting and visualizing these blocks, the indicator helps traders identify key levels where price might react, aiding in entry and exit decisions. The customizable settings allow traders to adjust the visibility and parameters to suit their specific trading strategy.

Liquidity Levels Analysis

Functionality: Liquidity levels indicate zones where significant price movements can occur due to the presence of large orders. These are areas where smart money might be executing trades.

Integration: By tracking these high-probability liquidity areas, traders can anticipate potential price movements. Customizable display limits and mitigation strategies ensure that the information is tailored to the trader’s needs, providing precise and actionable insights.

Fair Value Gaps (FVG)

Functionality: Fair value gaps highlight areas where there is an imbalance between buyers and sellers. These gaps often represent potential trading opportunities.

Integration: The ability to identify and analyze FVGs helps traders spot potential entries based on market inefficiencies. The touch and break detection functionalities provide further refinement, enhancing the precision of trading signals.

Trendlines

Functionality: Trendlines help in identifying the direction of the market and potential reversal points. The additional trendline adds a layer of confirmation for breaks or retests.

Integration: Automatically drawn trendlines assist traders in visualizing market trends and making decisions about potential entries and exits. The additional trendline for stronger confirmation reduces the risk of false signals, providing more reliable trading opportunities.

Market Structure Analysis

Functionality: Understanding market structure is crucial for identifying key support and resistance levels and overall market dynamics. This component displays internal, external, and composite market structures.

Integration: By automatically highlighting shifts in market structure, the indicator helps traders recognize important levels and potential changes in market direction. This analysis is critical for strategic planning and execution in trading.

Customizable Alerts

Functionality: Alerts ensure that traders do not miss significant market events, such as the formation or breach of order blocks, liquidity levels, and trendline interactions.

Integration: Customizable alerts enhance the user experience by providing timely notifications of key events. This feature ensures that traders can act quickly and efficiently, leveraging the insights provided by the indicator.

Interactive Visualization

Functionality: Customizable visual aspects of the indicator allow traders to tailor the display to their preferences and trading style.

Integration: This feature enhances user engagement and usability, making it easier for traders to interpret the data and make informed decisions. Personalization options like colors, styles, and display formats improve the overall effectiveness of the indicator.

How Components Work Together

Comprehensive Market Analysis

Each component of the indicator addresses a different aspect of market analysis. Order blocks and liquidity levels highlight potential support and resistance zones, while fair value gaps and trendlines provide additional context for potential entries and exits. Market structure analysis ties everything together by offering a broad view of market dynamics.

Synergistic Insights

The integration of multiple features allows for cross-validation of trading signals. For instance, an order block coinciding with a high-probability liquidity level and a fair value gap can provide a stronger signal than any of these features alone. This synergy enhances the reliability of the insights and trading signals generated by the indicator.

Enhanced Decision Making

By combining these advanced features into a single tool, traders are equipped with a powerful resource for making informed decisions. The customizable alerts and interactive visualization further support this by ensuring that traders can act quickly on the insights provided.

Order Blocks ( OB) & Breaker Blocks (BB) Visuals:

📝 OB Input Settings

📊 Timeframe #1

TF #1🕑: Enable or disable Timeframe 1.

What it is: A boolean input to toggle the use of the first timeframe.

What it does: Enables or disables Timeframe 1 for the OB settings.

How to use it: Check or uncheck the box to enable or disable.

📊 Timeframe 1 Selection

Timeframe #1🕑: Select the timeframe for Timeframe 1.

What it is: A dropdown to select the desired timeframe.

What it does: Sets the timeframe for Timeframe 1.

How to use it: Choose a timeframe from the dropdown list.

📊 Timeframe #2

TF #2🕑: Enable or disable Timeframe 2.

What it is: A boolean input to toggle the use of the second timeframe.

What it does: Enables or disables Timeframe 2 for the OB settings.

How to use it: Check or uncheck the box to enable or disable.

📊 Timeframe 2 Selection

Timeframe #2🕑: Select the timeframe for Timeframe 2.

What it is: A dropdown to select the desired timeframe.

What it does: Sets the timeframe for Timeframe 2.

How to use it: Choose a timeframe from the dropdown list.

Additional Info: Higher TF Chart & Lower TF Setting / Lower TF Chart & Higher TF Setting.

📏 Show OBs

OB (Length)📏: Toggle the display of Order Blocks.

What it is: A boolean input to enable or disable the display of Order Blocks.

What it does: Shows or hides Order Blocks based on the selected swing length.

How to use it: Check or uncheck the box to enable or disable.

📏 Swing Length Option

Swing Length Option: Select the swing length option.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of swings for Order Blocks.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=10, MID=28, LONG=50.

🔧 Custom Swing Length

🔧custom: Specify a custom swing length.

What it is: An integer input for setting a custom swing length.

What it does: Overrides the default swing lengths if set to CUSTOM.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

📛 Show BBs

BB (Method)📛: Toggle the display of Breaker Blocks.

What it is: A boolean input to enable or disable the display of Breaker Blocks.

What it does: Shows or hides Breaker Blocks.

How to use it: Check or uncheck the box to enable or disable.

📛 OB End Method

OB End Method: Select the method for determining the end of a Breaker Block.

What it is: A dropdown to choose between Wick and Close.

What it does: Sets the criteria for when a Breaker Block is considered mitigated.

How to use it: Choose an option from the dropdown.

Additional Info: Wicks: OB is mitigated when the price wicks through the OB Level. Close: OB is mitigated when the closing price is within the OB Level.

🔍 Max Bullish Zones

🔍Max Bullish: Set the maximum number of Bullish Order Blocks to display.

What it is: A dropdown to select the maximum number of Bullish Order Blocks.

What it does: Limits the number of Bullish Order Blocks shown on the chart.

How to use it: Choose a value from the dropdown (1-10).

🔍 Max Bearish Zones

🔍Max Bearish: Set the maximum number of Bearish Order Blocks to display.

What it is: A dropdown to select the maximum number of Bearish Order Blocks.

What it does: Limits the number of Bearish Order Blocks shown on the chart.

How to use it: Choose a value from the dropdown (1-10).

🟩 Bullish OB Color

Bullish OB Color: Set the color for Bullish Order Blocks.

What it is: A color picker to set the color of Bullish Order Blocks.

What it does: Changes the color of Bullish Order Blocks on the chart.

How to use it: Select a color from the color picker.

🟥 Bearish OB Color

Bearish OB Color: Set the color for Bearish Order Blocks.

What it is: A color picker to set the color of Bearish Order Blocks.

What it does: Changes the color of Bearish Order Blocks on the chart.

How to use it: Select a color from the color picker.

🔧 OB & BB Range

↔ OB & BB Range: Select the range option for OB and BB.

What it is: A dropdown to choose between RANGE and CUSTOM.

What it does: Sets how far the OB or BB should extend.

How to use it: Choose an option from the dropdown.

Additional Info: RANGE = Current price, CUSTOM = Adjustable Range.

🔧 Custom OB & BB Range

🔧Custom: Specify a custom range for OB and BB.

What it is: An integer input for setting a custom range.

What it does: Defines how far the OB or BB should go, based on a custom value.

How to use it: Enter a custom integer value (range: 1000-500000).

💬 Text Options

💬Text Options: Set text size and color for OB and BB.

What it is: A dropdown to select text size and a color picker to choose text color.

What it does: Changes the size and color of the text displayed for OB and BB.

How to use it: Select a size from the dropdown and a color from the color picker.

💬 Show Timeframe OB

Text: Toggle to display the timeframe of OB.

What it is: A boolean input to show or hide the timeframe text for OB.

What it does: Displays the timeframe information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

💬 Show Volume

Volume: Toggle to display the volume of OB.

What it is: A boolean input to show or hide the volume information for Order Blocks.

What it does: Displays the volume information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The volume displayed represents the total trading volume that occurred during the formation of the Order Block. This can indicate the level of participation or interest in that price level.

How it's calculated: The volume is the sum of all traded volumes within the candles that form the Order Block.

What it means: Higher volume at an Order Block level may suggest stronger support or resistance. It shows the amount of trading activity and can be an indicator of the potential strength or validity of the Order Block.

Why it's shown: To give traders an idea of the market participation and to help assess the strength of the Order Block.

💬 Show Percentage

%: Toggle to display the percentage of OB.

What it is: A boolean input to show or hide the percentage information for Order Blocks.

What it does: Displays the percentage information for Order Blocks on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The percentage displayed usually represents the proportion of price movement relative to the Order Block.

How it's calculated: This can be the percentage move from the start to the end of the Order Block or the retracement level that price has reached relative to the Order Block's range.

What it means: It helps traders understand the extent of price movement within the Order Block and can indicate the significance of the price level.

Why it's shown: To provide a clearer understanding of the price dynamics and the importance of the Order Block within the overall price movement.

Additional Information

Volume Example: If an Order Block forms over three candles with volumes of 100, 150, and 200, the total volume displayed for that Order Block would be 450.

Percentage Example: If the price moves from 100 to 110 within an Order Block, and the total range of the Order Block is from 100 to 120, the percentage shown might be 50% (since the price has moved halfway through the Order Block's range).

Liquidity Levels visuals:

📊 Liquidity Levels Input Settings

📊 Current Timeframe

TF #1🕑: Enable or disable the current timeframe.

What it is: A boolean input to toggle the use of the current timeframe.

What it does: Enables or disables the display of liquidity levels for the current timeframe.

How to use it: Check or uncheck the box to enable or disable.

📊 Higher Timeframe

Higher Timeframe: Select the higher timeframe for liquidity levels.

What it is: A dropdown to select the desired higher timeframe.

What it does: Sets the higher timeframe for liquidity levels.

How to use it: Choose a timeframe from the dropdown list.

📏 Liquidity Length Option

📏Liquidity Length: Select the length for liquidity levels.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of swings for liquidity levels.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=10, MID=28, LONG=50.

🔧 Custom Liquidity Length

🔧custom: Specify a custom length for liquidity levels.

What it is: An integer input for setting a custom swing length.

What it does: Overrides the default liquidity lengths if set to CUSTOM.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

📛 Mitigation Method

📛Mitigation (Method): Select the method for determining the mitigation of liquidity levels.

What it is: A dropdown to choose between Close and Wick.

What it does: Sets the criteria for when a liquidity level is considered mitigated.

How to use it: Choose an option from the dropdown.

Additional Info:

Wick: Level is mitigated when the price wicks through the level.

Close: Level is mitigated when the closing price is within the level.

📛 Display Mitigated Levels

-: Select to display or hide mitigated levels.

What it is: A dropdown to choose between Remove and Show.

What it does: Displays or hides mitigated liquidity levels.

How to use it: Choose an option from the dropdown.

Additional Info:

Remove: Hide mitigated levels.

Show: Display mitigated levels.

🔍 Max Buy Side Liquidity

🔍Max Buy Side Liquidity: Set the maximum number of Buy Side Liquidity Levels to display.

What it is: An integer input to set the maximum number of Buy Side Liquidity Levels.

What it does: Limits the number of Buy Side Liquidity Levels shown on the chart.

How to use it: Enter a value between 0 and 50.

🟦 Buy Side Liquidity Color

Buy Side Liquidity Color: Set the color for Buy Side Liquidity Levels.

What it is: A color picker to set the color of Buy Side Liquidity Levels.

What it does: Changes the color of Buy Side Liquidity Levels on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Buy Side Liquidity Levels to display. Default: 5, Min: 1, Max: 50.

If liquidity levels are not displayed as expected, try increasing the max count.

🔍 Max Sell Side Liquidity

🔍Max Sell Side Liquidity: Set the maximum number of Sell Side Liquidity Levels to display.

What it is: An integer input to set the maximum number of Sell Side Liquidity Levels.

What it does: Limits the number of Sell Side Liquidity Levels shown on the chart.

How to use it: Enter a value between 0 and 50.

🟥 Sell Side Liquidity Color

Sell Side Liquidity Color: Set the color for Sell Side Liquidity Levels.

What it is: A color picker to set the color of Sell Side Liquidity Levels.

What it does: Changes the color of Sell Side Liquidity Levels on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Sell Side Liquidity Levels to display. Default: 5, Min: 1, Max: 50.

If liquidity levels are not displayed as expected, try increasing the max count.

✂ Box Style (Height)

✂ Box Style (↕): Set the box height style for liquidity levels.

What it is: A float input to set the height of the boxes.

What it does: Adjusts the height of the boxes displaying liquidity levels.

How to use it: Enter a value between -50 and 50.

Additional Info: Default value is -5.

📏 Box Length

b: Set the box length of liquidity levels.

What it is: An integer input to set the length of the boxes.

What it does: Adjusts the length of the boxes displaying liquidity levels.

How to use it: Enter a value between 0 and 500.

Additional Info: Default value is 20.

⏭ Extend Liquidity Levels

Extend ⏭: Toggle to extend liquidity levels beyond the current range.

What it is: A boolean input to enable or disable the extension of liquidity levels.

What it does: Extends liquidity levels beyond their default range.

How to use it: Check or uncheck the box to enable or disable.

Additional Info: Extend liquidity levels beyond the current range.

💬 Text Options

💬 Text Options: Set text size and color for liquidity levels.

What it is: A dropdown to select text size and a color picker to choose text color.

What it does: Changes the size and color of the text displayed for liquidity levels.

How to use it: Select a size from the dropdown and a color from the color picker.

💬 Show Text

Text: Toggle to display text for liquidity levels.

What it is: A boolean input to show or hide the text for liquidity levels.

What it does: Displays the text information for liquidity levels on the chart.

How to use it: Check or uncheck the box to enable or disable.

💬 Show Volume

Volume: Toggle to display the volume of liquidity levels.

What it is: A boolean input to show or hide the volume information for liquidity levels.

What it does: Displays the volume information for liquidity levels on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The volume displayed represents the total trading volume that occurred during the formation of the liquidity level. This can indicate the level of participation or interest in that price level.

How it's calculated: The volume is the sum of all traded volumes within the candles that form the liquidity level.

What it means: Higher volume at a liquidity level may suggest stronger support or resistance. It shows the amount of trading activity and can be an indicator of the potential strength or validity of the liquidity level.

Why it's shown: To give traders an idea of the market participation and to help assess the strength of the liquidity level.

💬 Show Percentage

%: Toggle to display the percentage of liquidity levels.

What it is: A boolean input to show or hide the percentage information for liquidity levels.

What it does: Displays the percentage information for liquidity levels on the chart.

How to use it: Check or uncheck the box to enable or disable.

Additional Info:

What it represents: The percentage displayed usually represents the proportion of price movement relative to the liquidity level.

How it's calculated: This can be the percentage move from the start to the end of the liquidity level or the retracement level that price has reached relative to the liquidity level's range.

What it means: It helps traders understand the extent of price movement within the liquidity level and can indicate the significance of the price level.

Why it's shown: To provide a clearer understanding of the price dynamics and the importance of the liquidity level within the overall price movement.

Fair Value Gaps visuals:

📊 Fair Value Gaps Input Settings

📊 Show FVG

TF #1🕑: Enable or disable Fair Value Gaps for Timeframe 1.

What it is: A boolean input to toggle the display of Fair Value Gaps.

What it does: Shows or hides Fair Value Gaps on the chart.

How to use it: Check or uncheck the box to enable or disable.

📊 Select Timeframe

Timeframe: Select the timeframe for Fair Value Gaps.

What it is: A dropdown to select the desired timeframe.

What it does: Sets the timeframe for Fair Value Gaps.

How to use it: Choose a timeframe from the dropdown list.

Additional Info: Higher TF Chart & Lower TF Setting or Lower TF Chart & Higher TF Setting.

📛 FVG Break Method

📛FVG Break (Method): Select the method for determining when an FVG is mitigated.

What it is: A dropdown to choose between Touch, Wicks, Close, or Average.

What it does: Sets the criteria for when a Fair Value Gap is considered mitigated.

How to use it: Choose an option from the dropdown.

Additional Info:

Touch: FVG is mitigated when the price touches the gap.

Wicks: FVG is mitigated when the price wicks through the gap.

Close: FVG is mitigated when the closing price is within the gap.

Average: FVG is mitigated when the average price (average of high and low) is within the gap.

📛 Show Mitigated FVG

show: Toggle to display mitigated FVGs.

What it is: A boolean input to show or hide mitigated Fair Value Gaps.

What it does: Displays or hides mitigated Fair Value Gaps.

How to use it: Check or uncheck the box to enable or disable.

📛 Fill FVG

Fill: Toggle to fill Fair Value Gaps.

What it is: A boolean input to fill the Fair Value Gaps with color.

What it does: Adds a color fill to the Fair Value Gaps.

How to use it: Check or uncheck the box to enable or disable.

📛 Shade FVG

Shade: Toggle to shade Fair Value Gaps.

What it is: A boolean input to shade the Fair Value Gaps.

What it does: Adds a shade effect to the Fair Value Gaps.

How to use it: Check or uncheck the box to enable or disable.

Additional Info: Select the method to break FVGs and toggle the visibility of FVG Breaks (fill FVG and/or shade FVG).

🔍 Max Bullish FVG

🔍Max Bullish FVG: Set the maximum number of Bullish Fair Value Gaps to display.

What it is: An integer input to set the maximum number of Bullish Fair Value Gaps.

What it does: Limits the number of Bullish Fair Value Gaps shown on the chart.

How to use it: Enter a value between 0 and 50.

🔍 Max Bearish FVG

🔍Max Bearish FVG: Set the maximum number of Bearish Fair Value Gaps to display.

What it is: An integer input to set the maximum number of Bearish Fair Value Gaps.

What it does: Limits the number of Bearish Fair Value Gaps shown on the chart.

How to use it: Enter a value between 0 and 50.

🟥 Bearish FVG Color

Bearish FVG Color: Set the color for Bearish Fair Value Gaps.

What it is: A color picker to set the color of Bearish Fair Value Gaps.

What it does: Changes the color of Bearish Fair Value Gaps on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Bearish Fair Value Gaps to display. Default: 5, Min: 1, Max: 50.

If Fair Value Gaps are not displayed as expected, try increasing the max count.

🟦 Bullish FVG Color

Bullish FVG Color: Set the color for Bullish Fair Value Gaps.

What it is: A color picker to set the color of Bullish Fair Value Gaps.

What it does: Changes the color of Bullish Fair Value Gaps on the chart.

How to use it: Select a color from the color picker.

Additional Info:

Tooltip: Set the maximum number of Bullish Fair Value Gaps to display. Default: 5, Min: 1, Max: 50.

If Fair Value Gaps are not displayed as expected, try increasing the max count.

📏 FVG Range

↔ FVG Range: Set the range for Fair Value Gaps.

What it is: An integer input to set the range of the Fair Value Gaps.

What it does: Adjusts the range of the Fair Value Gaps displayed.

How to use it: Enter a value between 0 and 100.

Additional Info: Adjustable length only works when both RANGE & EXTEND display OFF. Range=current price, Extend=Full Range.

⏭ Extend FVG

Extend⏭: Toggle to extend Fair Value Gaps beyond the current range.

What it is: A boolean input to enable or disable the extension of Fair Value Gaps.

What it does: Extends Fair Value Gaps beyond their default range.

How to use it: Check or uncheck the box to enable or disable.

⏯ FVG Range

Range⏯: Toggle the range of Fair Value Gaps.

What it is: A boolean input to enable or disable the range display for Fair Value Gaps.

What it does: Sets the range of Fair Value Gaps displayed.

How to use it: Check or uncheck the box to enable or disable.

↕ Max Width

↕ Max Width: Set the maximum width of Fair Value Gaps.

What it is: A float input to set the maximum width of Fair Value Gaps.

What it does: Limits the width of Fair Value Gaps as a percentage of the price range.

How to use it: Enter a value between 0 and 5.0.

Additional Info: FVGs wider than this value will be ignored.

♻ Filter FVG

Filter FVG ♻: Toggle to filter out small Fair Value Gaps.

What it is: A boolean input to filter out small Fair Value Gaps.

What it does: Ignores Fair Value Gaps smaller than the specified max width.

How to use it: Check or uncheck the box to enable or disable.

➖ Mid Line Style

➖Mid Line Style: Select the style of the mid line for Fair Value Gaps.

What it is: A dropdown to choose between Solid, Dashed, or Dotted.

What it does: Sets the style of the mid line within Fair Value Gaps.

How to use it: Choose an option from the dropdown.

🎨 Mid Line Color

Mid Line Color: Set the color for the mid line within Fair Value Gaps.

What it is: A color picker to set the color of the mid line.

What it does: Changes the color of the mid line within Fair Value Gaps.

How to use it: Select a color from the color picker.

Additional Information

Mitigation Methods: Each method (Touch, Wicks, Close, Average) provides different criteria for when a Fair Value Gap is considered mitigated, helping traders to understand the dynamics of price movements within gaps.

Volume and Percentage: Displaying volume and percentage information for Fair Value Gaps helps traders gauge the strength and significance of these gaps in relation to trading activity and price movements.

Trendlines visuals:

📊 Trendlines Input Settings

📊 Show Trendlines

Trendlines & Trendlines Difference(%) ↕: Enable or disable trendlines and set the percentage difference from the first trendline.

What it is: A boolean input to toggle the display of trendlines.

What it does: Shows or hides trendlines on the chart and allows setting a percentage difference from the first trendline.

How to use it: Check or uncheck the box to enable or disable.

Additional Info: The percentage difference determines the distance of the second trendline from the first one.

📏 Trendline Length Option

📏Trendline Length: Select the length for trendlines.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of trendlines.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=50, MID=100, LONG=200.

🔧 Custom Trendline Length

🔧custom: Specify a custom length for trendlines.

What it is: An integer input for setting a custom trendline length.

What it does: Overrides the default trendline lengths if set to CUSTOM.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

🔍 Max Bearish Trendlines

🔍Max Trendlines Bearish: Set the maximum number of bearish trendlines to display.

What it is: A dropdown to select the maximum number of bearish trendlines.

What it does: Limits the number of bearish trendlines shown on the chart.

How to use it: Choose a value from the dropdown (2-20).

🟩 Bearish Trendline Color

Bearish Trendline Color: Set the color for bearish trendlines.

What it is: A color picker to set the color of bearish trendlines.

What it does: Changes the color of bearish trendlines on the chart.

How to use it: Select a color from the color picker.

Additional Info: Adjust to control how many bearish trendlines are displayed.

🔍 Max Bullish Trendlines

🔍Max Trendlines Bullish: Set the maximum number of bullish trendlines to display.

What it is: A dropdown to select the maximum number of bullish trendlines.

What it does: Limits the number of bullish trendlines shown on the chart.

How to use it: Choose a value from the dropdown (2-20).

🟥 Bullish Trendline Color

Bullish Trendline Color: Set the color for bullish trendlines.

What it is: A color picker to set the color of bullish trendlines.

What it does: Changes the color of bullish trendlines on the chart.

How to use it: Select a color from the color picker.

Additional Info: Adjust to control how many bullish trendlines are displayed.

📐 Degrees Text

📐Degrees ° (💬 Size): Enable or disable degrees text and set its size and color.

What it is: A boolean input to show or hide the degrees text for trendlines.

What it does: Displays the degrees text for trendlines.

How to use it: Check or uncheck the box to enable or disable.

📏 Text Size for Degrees

Text Size: Set the text size for degrees on trendlines.

What it is: A dropdown to select the size of the degrees text.

What it does: Changes the size of the degrees text displayed for trendlines.

How to use it: Choose a size from the dropdown (XS, S, M, L, XL).

🎨 Degrees Text Color

Degrees Text Color: Set the color for the degrees text on trendlines.

What it is: A color picker to set the color of the degrees text.

What it does: Changes the color of the degrees text on the chart.

How to use it: Select a color from the color picker.

♻ Filter Degrees

♻ Filter Degrees °: Enable or disable angle filtering and set the angle range.

What it is: A boolean input to filter trendlines by their angle.

What it does: Shows only trendlines within a specified angle range.

How to use it: Check or uncheck the box to enable or disable.

Additional Info: Angles outside this range will be filtered out.

🔢 Angle Range

Angle Range: Set the angle range for filtering trendlines.

What it is: Two float inputs to set the minimum and maximum angle for trendlines.

What it does: Defines the range of angles for which trendlines will be shown.

How to use it: Enter values for the minimum and maximum angles.

➖ Line Style

➖Style #1 & #2: Select the style of the primary and secondary trendlines.

What it is: Two dropdowns to choose between Solid, Dashed, or Dotted for the trendlines.

What it does: Sets the style of the primary and secondary trendlines.

How to use it: Choose a style from each dropdown.

📏 Line Thickness

: Set the thickness for the trendlines.

What it is: An integer input to set the thickness of the trendlines.

What it does: Adjusts the thickness of the trendlines displayed on the chart.

How to use it: Enter a value between 1 and 5.

Additional Information

Trendline Percentage Difference: Setting a percentage difference helps in analyzing the relative position and angle of trendlines.

Filtering by Angle: This feature allows focusing on trendlines within a specific angle range, enhancing the clarity of trend analysis.

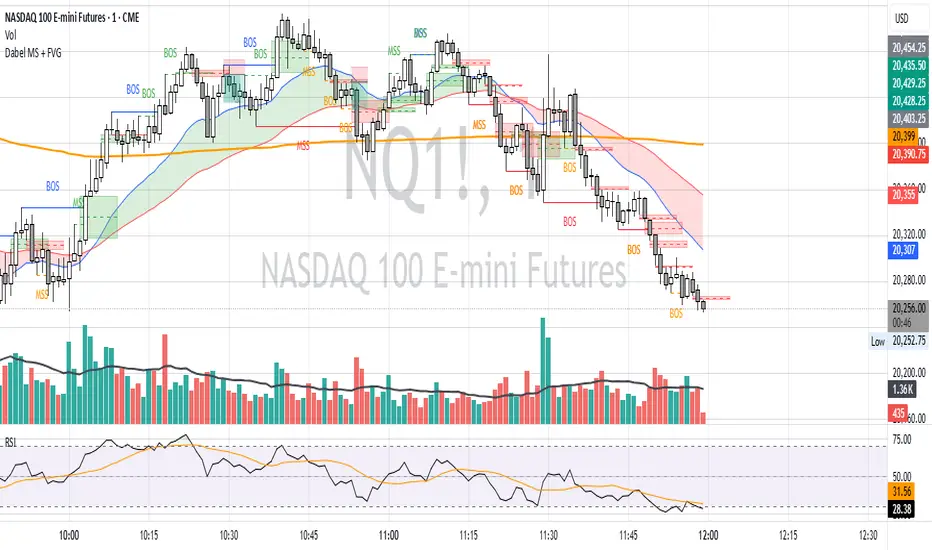

BOS & CHOCH Market Structure visuals:

📊 BOS & CHOCH Market Structure Input Settings

📏 Market Structure Length Option

📏Market Structure: Select the market structure length option.

What it is: A dropdown to choose between INTERNAL, EXTERNAL, ALL, CUSTOM, or NONE.

What it does: Sets the type of market structure to be displayed.

How to use it: Choose an option from the dropdown.

Additional Info:

INTERNAL: Only internal structure.

EXTERNAL: Only external structure.

ALL: Both internal and external structures.

CUSTOM: Custom lengths.

NONE: No structure.

🔧 Custom Internal Length

🔧Custom Internal: Specify a custom length for internal market structure.

What it is: An integer input for setting a custom internal length.

What it does: Defines the length of internal market structures if CUSTOM is selected.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

💬 Internal Label Size

💬Internal Label Size: Set the label size for internal market structures.

What it is: A dropdown to select the size of the labels.

What it does: Changes the size of the labels for internal market structures.

How to use it: Choose a size from the dropdown (XS, S, M, L, XL).

🟩 Internal Bullish Color

Internal Bullish Color: Set the color for bullish internal market structures.

What it is: A color picker to set the color of bullish internal market structures.

What it does: Changes the color of bullish internal market structures on the chart.

How to use it: Select a color from the color picker.

🟥 Internal Bearish Color

Internal Bearish Color: Set the color for bearish internal market structures.

What it is: A color picker to set the color of bearish internal market structures.

What it does: Changes the color of bearish internal market structures on the chart.

How to use it: Select a color from the color picker.

🔧 Custom External Length

🔧Custom External: Specify a custom length for external market structure.

What it is: An integer input for setting a custom external length.

What it does: Defines the length of external market structures if CUSTOM is selected.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

💬 External Label Size

💬External Label Size: Set the label size for external market structures.

What it is: A dropdown to select the size of the labels.

What it does: Changes the size of the labels for external market structures.

How to use it: Choose a size from the dropdown (XS, S, M, L, XL).

🟩 External Bullish Color

External Bullish Color: Set the color for bullish external market structures.

What it is: A color picker to set the color of bullish external market structures.

What it does: Changes the color of bullish external market structures on the chart.

How to use it: Select a color from the color picker.

🟥 External Bearish Color

External Bearish Color: Set the color for bearish external market structures.

What it is: A color picker to set the color of bearish external market structures.

What it does: Changes the color of bearish external market structures on the chart.

How to use it: Select a color from the color picker.

📐 Show Equal Highs and Lows

EQL & EQH📐: Toggle visibility for equal highs and lows.

What it is: A boolean input to show or hide equal highs and lows.

What it does: Displays or hides equal highs and lows on the chart.

How to use it: Check or uncheck the box to enable or disable.

📏 Equal Highs and Lows Threshold

Equal Highs and Lows Threshold: Set the threshold for equal highs and lows.

What it is: A float input to set the threshold for equal highs and lows.

What it does: Defines the range within which highs and lows are considered equal.

How to use it: Enter a value between 0 and 10.

💬 Label Size for Equal Highs and Lows

💬Label Size for Equal Highs and Lows: Set the label size for equal highs and lows.

What it is: A dropdown to select the size of the labels.

What it does: Changes the size of the labels for equal highs and lows.

How to use it: Choose a size from the dropdown (XS, S, M, L, XL).

🟩 Bullish Color for Equal Highs and Lows

Bullish Color for Equal Highs and Lows: Set the color for bullish equal highs and lows.

What it is: A color picker to set the color of bullish equal highs and lows.

What it does: Changes the color of bullish equal highs and lows on the chart.

How to use it: Select a color from the color picker.

🟥 Bearish Color for Equal Highs and Lows

Bearish Color for Equal Highs and Lows: Set the color for bearish equal highs and lows.

What it is: A color picker to set the color of bearish equal highs and lows.

What it does: Changes the color of bearish equal highs and lows on the chart.

How to use it: Select a color from the color picker.

📏 Show Swing Points

Swing Points📏: Toggle visibility for swing points.

What it is: A boolean input to show or hide swing points.

What it does: Displays or hides swing points on the chart.

How to use it: Check or uncheck the box to enable or disable.

📏 Swing Points Length Option

Swing Points Length Option: Select the length for swing points.

What it is: A dropdown to choose between SHORT, MID, LONG, or CUSTOM.

What it does: Sets the length of swing points.

How to use it: Choose an option from the dropdown.

Additional Info: Default lengths are SHORT=10, MID=28, LONG=50.

💬 Swing Points Label Size

💬Swing Points Label Size: Set the label size for swing points.

What it is: A dropdown to select the size of the labels.

What it does: Changes the size of the labels for swing points.

How to use it: Choose a size from the dropdown (XS, S, M, L, XL).

🎨 Swing Points Color

Swing Points Color: Set the color for swing points.

What it is: A color picker to set the color of swing points.

What it does: Changes the color of swing points on the chart.

How to use it: Select a color from the color picker.

🔧 Custom Swing Points Length

🔧Custom Swings: Specify a custom length for swing points.

What it is: An integer input for setting a custom length for swing points.

What it does: Defines the length of swing points if CUSTOM is selected.

How to use it: Enter a custom integer value (only shown when CUSTOM is selected).

Additional Information

Market Structure Types: Understanding internal and external structures helps in analyzing different market behaviors.

Equal Highs and Lows: This feature identifies areas where price action is balanced, which can be significant for trading strategies.

Swing Points: Highlighting swing points aids in recognizing significant market reversals or continuations.

Benefits

Enhance your trading strategy by visualizing smart money's influence on price movements.

Make informed decisions with real-time data on significant market structures.

Reduce manual analysis with automated detection of key trading signals.

Ideal For

Traders looking for an edge in forex, equities, and cryptocurrency markets by understanding the underlying forces driving market dynamics.

Acknowledgements

Special thanks to these amazing creators for inspiration and their creations:

I want to thank these amazing creators for creating there amazing indicators , that inspired me and also gave me a head start by making this indicator! Without their amazing indicators it wouldn't be possible!

Flux Charts: Volumized Order Blocks

LuxAlgo: Trend Lines

UAlgo: Fair Value Gaps (FVG)

By Leviathan: Market Structure

Sonarlab: Liquidity Levels

Note

Remember to always backtest the indicator first before integrating it into your strategy! For any questions about the indicator, please feel free to ask for assistance.

Pure Price Action Structures [LuxAlgo]The Pure Price Action Structures indicator is a pure price action analysis tool designed to automatically identify real-time market structures.

The indicator identifies short-term, intermediate-term, and long-term swing highs and lows, forming the foundation for real-time detection of shifts and breaks in market structure.

Its distinctive/unique feature lies in its reliance solely on price patterns, without being limited by any user-defined input, ensuring a robust and objective analysis of market dynamics.

🔶 USAGE

Market structure is a crucial aspect of understanding price action. The script automatically identifies real-time market structure, enabling traders to comprehend market trends more easily. It assists traders in recognizing both trend changes and continuations.

Market structures are constructed from three sets of swing points, short-term swings, intermediary swings, and long-term swings. Market structures associated with longer-term swing points are indicative of longer-term trends.

A market structure shift (MSS), also known as a change of character (CHoCH), is a significant event in price action analysis that may signal a potential shift in market sentiment or direction. Conversely, a break of structure (BOS) is another significant event in price action analysis that typically indicates a continuation of the prevailing trend.

However, it's important to note that while an MSS can be the first indication of a trend reversal and a BOS signifies a continuation of the prevailing trend, they do not guarantee a complete reversal or continuation of the trend.

In some cases, MSS and BOS levels may also act as liquidity zones or areas of price consolidation, rather than indicating a definitive change in market direction or continuation. Traders should approach them with caution and consider additional factors to confirm the validity of the signal before making trading decisions.

🔶 DETAILS

🔹 Market Structures

Market structures are based on the analysis of price action and aim to identify key levels and patterns in the market, where swing point detection is one of the core concepts within ICT trading methodologies and teachings.

Swing points are automatically detected solely based on market movements, without any reliance on user-defined input.

🔹 Utilizing Swing Points

Swing points are not identified in real time as they occur. While short-term swing points may be displayed with a delay of at most one bar, the identification of intermediate and long-term swing points depends entirely on market movements. Furthermore, detection is not limited by any user-defined input but relies solely on pure price action. Consequently, swing points are not typically utilized in real-time trading scenarios.

Traders often analyze historical swing points to discern market trends and pinpoint potential entry and exit points for their trades. By identifying swing highs and lows, traders can:

Recognize Trends: Swing highs and lows help traders identify the direction of the trend. Higher swing highs and higher swing lows indicate an uptrend, while lower swing highs and lower swing lows indicate a downtrend.

Identify Support and Resistance Levels: Swing highs often serve as resistance levels, known in ICT terminology as Buyside Liquidity Levels, while swing lows function as support levels, also referred to in ICT terminology as Sellside Liquidity Levels. Traders can utilize these levels to strategize entry and exit points for their trades.

Spot Reversal Patterns: Swing points can form various reversal patterns, such as double tops or bottoms, head and shoulders patterns, and triangles. Recognizing these patterns can signal potential trend reversals, allowing traders to adjust their strategies accordingly.

Set Stop Loss and Take Profit Levels: In the context of ICT teachings, swing levels represent specific price levels where a concentration of buy or sell orders is anticipated. Traders can target these liquidity levels/pools to accumulate or distribute their positions, essentially using swing points to establish stop loss and take profit levels for their trades.

Overall, swing points provide valuable information about market dynamics and can assist traders in making more informed trading decisions.

🔶 SETTINGS

🔹 Structures

Swings and Size: Toggles the visibility of the structure's highs and lows, assigns an icon corresponding to the structures, and controls the size of the icons.

Market Structures: Toggles the visibility of the market structures.

Market Structure Labels: Controls the visibility of labels that highlight the type of market structure.

Line Style and Width: Customizes the style and width of the lines representing the market structure.

Swing and Line Colors: Customizes colors for the icons representing highs and lows, and the lines and labels representing the market structure.

🔶 RELATED SCRIPTS

Market-Structures-(Intrabar).

Buyside-Sellside-Liquidity.

Pure Price Action ICT Tools [LuxAlgo]The Pure Price Action ICT Tools indicator is designed for pure price action analysis, automatically identifying real-time market structures, liquidity levels, order & breaker blocks, and liquidity voids.

Its unique feature lies in its exclusive reliance on price patterns, without being constrained by any user-defined inputs, ensuring a robust and objective analysis of market dynamics.

🔶 MARKET STRUCTURES

A Market Structure Shift, also known as a Change of Character (CHoCH), is a pivotal event in price action analysis indicating a potential change in market sentiment or direction. An MSS occurs when the price reverses from an established trend, signaling that the prevailing trend may be losing momentum and a reversal might be underway. This shift is often identified by key technical patterns, such as a higher low in a downtrend or a lower high in an uptrend, which indicate a weakening of the current trend's strength.

A Break of Structure typically indicates the continuation of the current market trend. This event occurs when the price decisively moves beyond a previous swing high or low, confirming the strength of the prevailing trend. In an uptrend, a BOS is marked by the price breaking above a previous high, while in a downtrend, it is identified by the price breaking below a previous low.

While a Market Structure Shift (MSS) can indicate a potential trend reversal and a Break of Structure (BOS) often confirms trend continuation, they do not assure a complete reversal or continuation. MSS and BOS levels can also function as liquidity zones or areas of price consolidation rather than definitively signaling a change in market direction. Traders should approach these signals cautiously and validate them with additional factors before making trading decisions. For further details on other components of the tool, please refer to the following sections.

🔶 ORDER & BREAKER BLOCKS

Order and Breaker Blocks are key concepts in price action analysis that help traders identify significant levels in the market structure.

Order Blocks are specific price zones where significant buying or selling activity has occurred. These zones often represent the actions of large institutional traders or market makers, who execute substantial orders that impact the market.

Breaker Blocks are specific price zones where a strong reversal occurs, causing a break in the prevailing market structure. These blocks indicate areas where the price encountered significant resistance or support, leading to a reversal.

In summary, Order and Breaker Blocks are essential tools in price action analysis, providing insights into significant market levels influenced by institutional trading activities. These blocks help traders make informed decisions about potential support and resistance levels, trend reversals, and breakout confirmations.

🔶 BUYSIDE & SELLSIDE LIQUIDITY

Both buy-side and sell-side liquidity zones are critical for identifying potential turning points in the market. These zones are where significant buying or selling interest is concentrated, influencing future price movements.

In summary, buy-side and sell-side liquidity provide crucial insights into market demand and supply dynamics, helping traders make informed decisions based on the availability of orders at different price levels.

🔶 LIQUIDITY VOIDS

Liquidity voids are gaps or areas on a price chart where there is a lack of trading activity. These voids represent zones with minimal to no buy or sell orders, often resulting in sharp price movements when the market enters these areas.

In summary, liquidity voids are crucial areas on a price chart characterized by a lack of trading activity. These voids can lead to rapid price movements and increased volatility, making them essential considerations for traders in their analysis and decision-making processes.

🔶 SWING POINTS

Reversal price points are commonly referred to as swing points. Traders often analyze historical swing points to discern market trends and pinpoint potential trade entry and exit points.

Do note that in this script these are subject to backpainting, that is they are not located where they are detected.

The detection of swing points and the unique feature of this script rely exclusively on price action, eliminating the need for numerical user-defined settings. The process begins with detecting short-term swing points:

Short-Term Swing High (STH): Identified as a price peak surrounded by lower highs on both sides.

Short-Term Swing Low (STL): Recognized as a price trough surrounded by higher lows on both sides.

Intermediate-term and long-term swing points are detected using the same approach but with a slight modification. Instead of directly analyzing price candles, previously detected short-term swing points are utilized. For intermediate-term swing points, short-term swing points are analyzed, while for long-term swing points, intermediate-term ones are used.

This method ensures a robust and objective analysis of market dynamics, offering traders reliable insights into market structures. Detected swing points serve as the foundation for identifying market structures, buy-side/sell-side liquidity levels, and order and breaker blocks presented with this tool.

In summary, swing points are essential elements in technical analysis, helping traders identify trends, support, and resistance levels, and optimal entry and exit points. Understanding swing points allows traders to make informed decisions based on the natural price movements in the market.

🔶 SETTINGS

🔹 Market Structures

Market Structures: Toggles the visibility of the market structures, both shifts and breaks.

Detection: An option that allows users to detect market structures based on the significance of swing levels, including short-term, intermediate-term, and long-term.

Market Structure Labels: Controls the visibility of labels that highlight the type of market structure.

Line Style: Customizes the style of the lines representing the market structure.

🔹 Order & Breaker Blocks

Order & Breaker Blocks: Toggles the visibility of the order & breaker blocks.

Detection: An option that allows users to detect order & breaker blocks based on the significance of swing levels, including short-term, intermediate-term, and long-term.

Last Bullish Blocks: Number of the most recent bullish order/breaker blocks to display on the chart.

Last Bearish Blocks: Number of the most recent bearish order/breaker blocks to display on the chart.

Use Candle Body: Allows users to use candle bodies as order block areas instead of the full candle range.

🔹 Buyside & Sellside Liquidity

Buyside & Sellside Liquidity: Toggles the visibility of the buyside & sellside liquidity levels.

Detection: An option that allows users to detect buy-side & sell-side liquidity based on the significance of swing levels, including short-term, intermediate-term, and long-term.

Margin: Sets margin/sensitivity for a liquidity level detection.

Visible Levels: Controls the amount of the liquidity levels/zones to be visualized.

🔹 Liquidity Voids

Liquidity Voids: Enable display of both bullish and bearish liquidity voids.

Threshold Multiplier: Defines the multiplier for the threshold, which is hard-coded to the 200-period ATR range.

Mode: Controls the lookback length for detection and visualization. Present considers the last X bars specified in the option, while Historical includes all available data.

Label: Enable display of a label indicating liquidity voids.

🔹 Swing Highs/Lows

Swing Highs/Lows: Toggles the visibility of the swing levels.

Detection: An option that allows users to detect swing levels based on the significance of swing levels, including short-term, intermediate-term, and long-term.

Label Size: Control the size of swing level labels.

🔶 RELATED SCRIPTS

Pure-Price-Action-Structures.

Market-Structures-(Intrabar).

Buyside-Sellside-Liquidity.

Order-Breaker-Blocks.

PriceActionLibrary "PriceAction"

Hi all!

This library will help you to plot the market structure and liquidity. By now, the only part in the price action section is liquidity, but I plan to add more later on. The market structure will be split into two parts, 'Internal' and 'Swing' with separate pivot lengths. For these two trends it will show you:

• Break of structure (BOS)

• Change of character (CHoCH/CHoCH+) (mandatory)

• Equal high/low (EQH/EQL)

It's inspired by "Smart Money Concepts (SMC) " by LuxAlgo.

This library is now the same code as the code in my library 'MarketStructure', but it has evolved into a more price action oriented library than just a market structure library. This is more accurate and I will continue working on this library to keep it growing.

This code does not provide any examples, but you can look at my indicators 'Market structure' () and 'Order blocks' (), where I use the 'MarketStructure' library (which is the same code).

Market structure

Both of these market structures can be enabled/disabled by setting them to 'na'. The pivots lengths can be configured separately. The pivots found will be the 'base' of and will show you when price breaks it. When that happens a break of structure or a change of character will be created. The latest 5 pivots found within the current trends will be kept to take action on. They are cleared on a change of character, so nothing (break of structures or change of characters) can happen on pivots before a trend change. The internal market structure is shown with dashed lines and swing market structure is shown with solid lines.

Labels for a change of character can have either the text 'CHoCH' or 'CHoCH+'. A Change of Character plus is formed when price fails to form a higher high or a lower low before reversing. Note that a pivot that is created after the change of character might have a higher high or a lower low, thus not making the break a 'CHoCH+'. This is not changed after the pivot is found but is kept as is.

A break of structure is removed if an earlier pivot within the same trend is broken, i.e. another break of structure (with a longer distance) is created. Like in the images below, the first pivot (in the first image) is removed when an earlier pivot's higher price within the same trend is broken (the second image):

[image [https://www.tradingview.com/x/PRP6YtPA/

Equal high/lows have a configurable color setting and can be configured to be extended to the right. Equal high/lows are only possible if it's not been broken by price. A factor (percentage of width) of the Average True Length (of length 14) that the pivot must be within to to be considered an Equal high/low. Equal highs/lows can be of 2 pivots or more.

You are able to show the pivots that are used. "HH" (higher high), "HL" (higher low), "LH" (lower high), "LL" (lower low) and "H"/"L" (for pivots (high/low) when the trend has changed) are the labels used. There are also labels for break of structures ('BOS') and change of characters ('CHoCH' or 'CHoCH+'). The size of these texts is set in the 'FontSize' setting.

When programming I focused on simplicity and ease of read. I did not focus on performance, I will do so if it's a problem (haven't noticed it is one yet).

You can set alerts for when a change of character, break of structure or an equal high/low (new or an addition to a previously found) happens. The alerts that are fired are on 'once_per_bar_close' to avoid repainting. This has the drawback to alert you when the bar closes.

Price action

The indicator will create lines and zones for spotted liquidity. It will draw a line (with dotted style) at the price level that was liquidated, but it will also draw a zone from that level to the bar that broke the pivot high or low price. If that zone is large the liquidation is big and might be significant. This can be disabled in the settings. You can also change the confirmation candles (that does not close above or below the pivot level) needed after a liquidation and how many pivots back to look at.

The lines and boxes drawn will look like this if the color is orange:

Hope this is of help!

Will draw out the market structure for the disired pivot length.

Liqudity(liquidity)

Will draw liquidity.

Parameters:

liquidity (Liquidity) : The 'PriceAction.Liquidity' object.

Pivot(structure)

Sets the pivots in the structure.

Parameters:

structure (Structure)

PivotLabels(structure)

Draws labels for the pivots found.

Parameters:

structure (Structure)

EqualHighOrLow(structure)

Draws the boxes for equal highs/lows. Also creates labels for the pivots included.

Parameters:

structure (Structure)

BreakOfStructure(structure)

Will create lines when a break of strycture occures.

Parameters:

structure (Structure)

Returns: A boolean that represents if a break of structure was found or not.

ChangeOfCharacter(structure)

Will create lines when a change of character occures. This line will have a label with "CHoCH" or "CHoCH+".

Parameters:

structure (Structure)

Returns: A boolean that represents if a change of character was found or not.

VisualizeCurrent(structure)

Will create a box with a background for between the latest high and low pivots. This can be used as the current trading range (if the pivots broke strucure somehow).

Parameters:

structure (Structure)

StructureBreak

Holds drawings for a structure break.

Fields:

Line (series line) : The line object.

Label (series label) : The label object.

Pivot

Holds all the values for a found pivot.

Fields:

Price (series float) : The price of the pivot.

BarIndex (series int) : The bar_index where the pivot occured.

Type (series int) : The type of the pivot (-1 = low, 1 = high).

Time (series int) : The time where the pivot occured.

BreakOfStructureBroken (series bool) : Sets to true if a break of structure has happened.

LiquidityBroken (series bool) : Sets to true if a liquidity of the price level has happened.

ChangeOfCharacterBroken (series bool) : Sets to true if a change of character has happened.

Structure

Holds all the values for the market structure.

Fields:

LeftLength (series int) : Define the left length of the pivots used.

RightLength (series int) : Define the right length of the pivots used.

Type (series Type) : Set the type of the market structure. Two types can be used, 'internal' and 'swing' (0 = internal, 1 = swing).

Trend (series int) : This will be set internally and can be -1 = downtrend, 1 = uptrend.

EqualPivotsFactor (series float) : Set how the limits are for an equal pivot. This is a factor of the Average True Length (ATR) of length 14. If a low pivot is considered to be equal if it doesn't break the low pivot (is at a lower value) and is inside the previous low pivot + this limit.

ExtendEqualPivotsZones (series bool) : Set to true if you want the equal pivots zones to be extended.

ExtendEqualPivotsStyle (series string) : Set the style of equal pivot zones.

ExtendEqualPivotsColor (series color) : Set the color of equal pivot zones.

EqualHighs (array) : Holds the boxes for zones that contains equal highs.

EqualLows (array) : Holds the boxes for zones that contains equal lows.

BreakOfStructures (array) : Holds all the break of structures within the trend (before a change of character).

Pivots (array) : All the pivots in the current trend, added with the latest first, this is cleared when the trend changes.

FontSize (series int) : Holds the size of the font displayed.

AlertChangeOfCharacter (series bool) : Holds true or false if a change of character should be alerted or not.

AlertBreakOfStructure (series bool) : Holds true or false if a break of structure should be alerted or not.

AlerEqualPivots (series bool) : Holds true or false if equal highs/lows should be alerted or not.

Liquidity

Holds all the values for liquidity.

Fields:

LiquidityPivotsHigh (array) : All high pivots for liquidity.

LiquidityPivotsLow (array) : All low pivots for liquidity.

LiquidityConfirmationBars (series int) : The number of bars to confirm that a liquidity is valid.

LiquidityPivotsLookback (series int) : A number of pivots to look back for.

FontSize (series int) : Holds the size of the font displayed.

PriceAction

Holds all the values for the general price action and the market structures.

Fields:

Liquidity (Liquidity)

Swing (Structure) : Placeholder for all objects used for the swing market structure.

Internal (Structure) : Placeholder for all objects used for the internal market structure.

SMC Structures and FVGสวัสดีครับ! ผมจะอธิบายอินดิเคเตอร์ "SMC Structures and FVG + MACD" ที่คุณให้มาอย่างละเอียดในแต่ละส่วน เพื่อให้คุณเข้าใจการทำงานของมันอย่างถ่องแท้ครับ

อินดิเคเตอร์นี้เป็นการผสมผสานแนวคิดของ Smart Money Concept (SMC) ซึ่งเน้นการวิเคราะห์โครงสร้างตลาด (Market Structure) และ Fair Value Gap (FVG) เข้ากับอินดิเคเตอร์ MACD เพื่อใช้เป็นตัวกรองหรือตัวยืนยันสัญญาณ Choch/BoS (Change of Character / Break of Structure)

1. ภาพรวมอินดิเคเตอร์ (Overall Purpose)

อินดิเคเตอร์นี้มีจุดประสงค์หลักคือ:

ระบุโครงสร้างตลาด: ตีเส้นและป้ายกำกับ Choch (Change of Character) และ BoS (Break of Structure) บนกราฟโดยอัตโนมัติ

ผสานการยืนยันด้วย MACD: สัญญาณ Choch/BoS จะถูกพิจารณาก็ต่อเมื่อ MACD Histogram เกิดการตัดขึ้นหรือลง (Zero Cross) ในทิศทางที่สอดคล้องกัน

แสดง Fair Value Gap (FVG): หากเปิดใช้งาน จะมีการตีกล่อง FVG บนกราฟ

แสดงระดับ Fibonacci: คำนวณและแสดงระดับ Fibonacci ที่สำคัญตามโครงสร้างตลาดปัจจุบัน

ปรับตาม Timeframe: การคำนวณและการแสดงผลทั้งหมดจะปรับตาม Timeframe ที่คุณกำลังใช้งานอยู่โดยอัตโนมัติ

2. ส่วนประกอบหลักของโค้ด (Code Breakdown)

โค้ดนี้สามารถแบ่งออกเป็นส่วนหลัก ๆ ได้ดังนี้:

2.1 Inputs (การตั้งค่า)

ส่วนนี้คือตัวแปรที่คุณสามารถปรับแต่งได้ในหน้าต่างการตั้งค่าของอินดิเคเตอร์ (คลิกที่รูปฟันเฟืองข้างชื่ออินดิเคเตอร์บนกราฟ)

MACD Settings (ตั้งค่า MACD):

fast_len: ความยาวของ Fast EMA สำหรับ MACD (ค่าเริ่มต้น 12)

slow_len: ความยาวของ Slow EMA สำหรับ MACD (ค่าเริ่มต้น 26)

signal_len: ความยาวของ Signal Line สำหรับ MACD (ค่าเริ่มต้น 9)

= ta.macd(close, fast_len, slow_len, signal_len): คำนวณค่า MACD Line, Signal Line และ Histogram โดยใช้ราคาปิด (close) และค่าความยาวที่กำหนด

is_bullish_macd_cross: ตรวจสอบว่า MACD Histogram ตัดขึ้นเหนือเส้น 0 (จากค่าลบเป็นบวก)

is_bearish_macd_cross: ตรวจสอบว่า MACD Histogram ตัดลงใต้เส้น 0 (จากค่าบวกเป็นลบ)

Fear Value Gap (FVG) Settings:

isFvgToShow: (Boolean) เปิด/ปิดการแสดง FVG บนกราฟ

bullishFvgColor: สีสำหรับ Bullish FVG

bearishFvgColor: สีสำหรับ Bearish FVG

mitigatedFvgColor: สีสำหรับ FVG ที่ถูก Mitigate (ลดทอน) แล้ว

fvgHistoryNbr: จำนวน FVG ย้อนหลังที่จะแสดง

isMitigatedFvgToReduce: (Boolean) เปิด/ปิดการลดขนาด FVG เมื่อถูก Mitigate

Structures (โครงสร้างตลาด) Settings:

isStructBodyCandleBreak: (Boolean) หากเป็น true การ Break จะต้องเกิดขึ้นด้วย เนื้อเทียน ที่ปิดเหนือ/ใต้ Swing High/Low หากเป็น false แค่ไส้เทียนทะลุก็ถือว่า Break

isCurrentStructToShow: (Boolean) เปิด/ปิดการแสดงเส้นโครงสร้างตลาดปัจจุบัน (เส้นสีน้ำเงินในภาพตัวอย่าง)

pivot_len: ความยาวของแท่งเทียนที่ใช้ในการมองหาจุด Pivot (Swing High/Low) ยิ่งค่าน้อยยิ่งจับ Swing เล็กๆ ได้, ยิ่งค่ามากยิ่งจับ Swing ใหญ่ๆ ได้

bullishBosColor, bearishBosColor: สีสำหรับเส้นและป้าย BOS ขาขึ้น/ขาลง

bosLineStyleOption, bosLineWidth: สไตล์ (Solid, Dotted, Dashed) และความหนาของเส้น BOS

bullishChochColor, bearishChochColor: สีสำหรับเส้นและป้าย CHoCH ขาขึ้น/ขาลง

chochLineStyleOption, chochLineWidth: สไตล์ (Solid, Dotted, Dashed) และความหนาของเส้น CHoCH

currentStructColor, currentStructLineStyleOption, currentStructLineWidth: สี, สไตล์ และความหนาของเส้นโครงสร้างตลาดปัจจุบัน

structHistoryNbr: จำนวนการ Break (Choch/BoS) ย้อนหลังที่จะแสดง

Structure Fibonacci (จากโค้ดต้นฉบับ):

เป็นชุด Input สำหรับเปิด/ปิด, กำหนดค่า, สี, สไตล์ และความหนาของเส้น Fibonacci Levels ต่างๆ (0.786, 0.705, 0.618, 0.5, 0.382) ที่จะถูกคำนวณจากโครงสร้างตลาดปัจจุบัน

2.2 Helper Functions (ฟังก์ชันช่วยทำงาน)

getLineStyle(lineOption): ฟังก์ชันนี้ใช้แปลงค่า String ที่เลือกจาก Input (เช่น "─", "┈", "╌") ให้เป็นรูปแบบ line.style_ ที่ Pine Script เข้าใจ

get_structure_highest_bar(lookback): ฟังก์ชันนี้พยายามหา Bar Index ของแท่งเทียนที่ทำ Swing High ภายในช่วง lookback ที่กำหนด

get_structure_lowest_bar(lookback): ฟังก์ชันนี้พยายามหา Bar Index ของแท่งเทียนที่ทำ Swing Low ภายในช่วง lookback ที่กำหนด

is_structure_high_broken(...): ฟังก์ชันนี้ตรวจสอบว่าราคาปัจจุบันได้ Break เหนือ _structureHigh (Swing High) หรือไม่ โดยพิจารณาจาก _highStructBreakPrice (ราคาปิดหรือราคา High ขึ้นอยู่กับการตั้งค่า isStructBodyCandleBreak)

FVGDraw(...): ฟังก์ชันนี้รับ Arrays ของ FVG Boxes, Types, Mitigation Status และ Labels มาประมวลผล เพื่ออัปเดตสถานะของ FVG (เช่น ถูก Mitigate หรือไม่) และปรับขนาด/ตำแหน่งของ FVG Box และ Label บนกราฟ

2.3 Global Variables (ตัวแปรทั่วทั้งอินดิเคเตอร์)

เป็นตัวแปรที่ประกาศด้วย var ซึ่งหมายความว่าค่าของมันจะถูกเก็บไว้และอัปเดตในแต่ละแท่งเทียน (persists across bars)

structureLines, structureLabels: Arrays สำหรับเก็บอ็อบเจกต์ line และ label ของเส้น Choch/BoS ที่วาดบนกราฟ

fvgBoxes, fvgTypes, fvgLabels, isFvgMitigated: Arrays สำหรับเก็บข้อมูลของ FVG Boxes และสถานะต่างๆ

structureHigh, structureLow: เก็บราคาของ Swing High/Low ที่สำคัญของโครงสร้างตลาดปัจจุบัน

structureHighStartIndex, structureLowStartIndex: เก็บ Bar Index ของจุดเริ่มต้นของ Swing High/Low ที่สำคัญ

structureDirection: เก็บสถานะของทิศทางโครงสร้างตลาด (1 = Bullish, 2 = Bearish, 0 = Undefined)

fiboXPrice, fiboXStartIndex, fiboXLine, fiboXLabel: ตัวแปรสำหรับเก็บข้อมูลและอ็อบเจกต์ของเส้น Fibonacci Levels

isBOSAlert, isCHOCHAlert: (Boolean) ใช้สำหรับส่งสัญญาณ Alert (หากมีการตั้งค่า Alert ไว้)

2.4 FVG Processing (การประมวลผล FVG)

ส่วนนี้จะตรวจสอบเงื่อนไขการเกิด FVG (Bullish FVG: high < low , Bearish FVG: low > high )

หากเกิด FVG และ isFvgToShow เป็น true จะมีการสร้าง box และ label ใหม่เพื่อแสดง FVG บนกราฟ

มีการจัดการ fvgBoxes และ fvgLabels เพื่อจำกัดจำนวน FVG ที่แสดงตาม fvgHistoryNbr และลบ FVG เก่าออก

ฟังก์ชัน FVGDraw จะถูกเรียกเพื่ออัปเดตสถานะของ FVG (เช่น การถูก Mitigate) และปรับการแสดงผล

2.5 Structures Processing (การประมวลผลโครงสร้างตลาด)

Initialization: ที่ bar_index == 0 (แท่งเทียนแรกของกราฟ) จะมีการกำหนดค่าเริ่มต้นให้กับ structureHigh, structureLow, structureHighStartIndex, structureLowStartIndex

Finding Current High/Low: highest, highestBar, lowest, lowestBar ถูกใช้เพื่อหา High/Low ที่สุดและ Bar Index ของมันใน 10 แท่งล่าสุด (หรือทั้งหมดหากกราฟสั้นกว่า 10 แท่ง)

Calculating Structure Max/Min Bar: structureMaxBar และ structureMinBar ใช้ฟังก์ชัน get_structure_highest_bar และ get_structure_lowest_bar เพื่อหา Bar Index ของ Swing High/Low ที่แท้จริง (ไม่ใช่แค่ High/Low ที่สุดใน lookback แต่เป็นจุด Pivot ที่สมบูรณ์)

Break Price: lowStructBreakPrice และ highStructBreakPrice จะเป็นราคาปิด (close) หรือราคา Low/High ขึ้นอยู่กับ isStructBodyCandleBreak

isStuctureLowBroken / isStructureHighBroken: เงื่อนไขเหล่านี้ตรวจสอบว่าราคาได้ทำลาย structureLow หรือ structureHigh หรือไม่ โดยพิจารณาจากราคา Break, ราคาแท่งก่อนหน้า และ Bar Index ของจุดเริ่มต้นโครงสร้าง

Choch/BoS Logic (ส่วนสำคัญที่ถูกผสานกับ MACD):

if(isStuctureLowBroken and is_bearish_macd_cross): นี่คือจุดที่ MACD เข้ามามีบทบาท หากราคาทำลาย structureLow (สัญญาณขาลง) และ MACD Histogram เกิด Bearish Zero Cross (is_bearish_macd_cross เป็น true) อินดิเคเตอร์จะพิจารณาว่าเป็น Choch หรือ BoS

หาก structureDirection == 1 (เดิมเป็นขาขึ้น) หรือ 0 (ยังไม่กำหนด) จะตีเป็น "CHoCH" (เปลี่ยนทิศทางโครงสร้างเป็นขาลง)

หาก structureDirection == 2 (เดิมเป็นขาลง) จะตีเป็น "BOS" (ยืนยันโครงสร้างขาลง)

มีการสร้าง line.new และ label.new เพื่อวาดเส้นและป้ายกำกับ

structureDirection จะถูกอัปเดตเป็น 1 (Bullish)

structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow จะถูกอัปเดตเพื่อกำหนดโครงสร้างใหม่

else if(isStructureHighBroken and is_bullish_macd_cross): เช่นกันสำหรับขาขึ้น หากราคาทำลาย structureHigh (สัญญาณขาขึ้น) และ MACD Histogram เกิด Bullish Zero Cross (is_bullish_macd_cross เป็น true) อินดิเคเตอร์จะพิจารณาว่าเป็น Choch หรือ BoS

หาก structureDirection == 2 (เดิมเป็นขาลง) หรือ 0 (ยังไม่กำหนด) จะตีเป็น "CHoCH" (เปลี่ยนทิศทางโครงสร้างเป็นขาขึ้น)

หาก structureDirection == 1 (เดิมเป็นขาขึ้น) จะตีเป็น "BOS" (ยืนยันโครงสร้างขาขึ้น)

มีการสร้าง line.new และ label.new เพื่อวาดเส้นและป้ายกำกับ

structureDirection จะถูกอัปเดตเป็น 2 (Bearish)

structureHighStartIndex, structureLowStartIndex, structureHigh, structureLow จะถูกอัปเดตเพื่อกำหนดโครงสร้างใหม่

การลบเส้นเก่า: d.delete_line (หากไลบรารีทำงาน) จะถูกเรียกเพื่อลบเส้นและป้ายกำกับเก่าออกเมื่อจำนวนเกิน structHistoryNbr

Updating Structure High/Low (else block): หากไม่มีการ Break เกิดขึ้น แต่ราคาปัจจุบันสูงกว่า structureHigh หรือต่ำกว่า structureLow ในทิศทางที่สอดคล้องกัน (เช่น ยังคงเป็นขาขึ้นและทำ High ใหม่) structureHigh หรือ structureLow จะถูกอัปเดตเพื่อติดตาม High/Low ที่สุดของโครงสร้างปัจจุบัน

Current Structure Display:

หาก isCurrentStructToShow เป็น true อินดิเคเตอร์จะวาดเส้น structureHighLine และ structureLowLine เพื่อแสดงขอบเขตของโครงสร้างตลาดปัจจุบัน

Fibonacci Display:

หาก isFiboXToShow เป็น true อินดิเคเตอร์จะคำนวณและวาดเส้น Fibonacci Levels ต่างๆ (0.786, 0.705, 0.618, 0.5, 0.382) โดยอิงจาก structureHigh และ structureLow ของโครงสร้างตลาดปัจจุบัน

Alerts:

alertcondition: ใช้สำหรับตั้งค่า Alert ใน TradingView เมื่อเกิดสัญญาณ BOS หรือ CHOCH

plot(na):

plot(na) เป็นคำสั่งที่สำคัญในอินดิเคเตอร์ที่ไม่ได้ต้องการพล็อต Series ของข้อมูลบนกราฟ (เช่น ไม่ได้พล็อตเส้น EMA หรือ RSI) แต่ใช้วาดอ็อบเจกต์ (Line, Label, Box) โดยตรง

การมี plot(na) ช่วยให้ Pine Script รู้ว่าอินดิเคเตอร์นี้มีเอาต์พุตที่แสดงผลบนกราฟ แม้ว่าจะไม่ได้เป็น Series ที่พล็อตตามปกติก็ตาม

3. วิธีใช้งาน

คัดลอกโค้ดทั้งหมด ที่อยู่ในบล็อก immersive ด้านบน

ไปที่ TradingView และเปิดกราฟที่คุณต้องการ

คลิกที่เมนู "Pine Editor" ที่อยู่ด้านล่างของหน้าจอ

ลบโค้ดเดิมที่มีอยู่ และ วางโค้ดที่คัดลอกมา ลงไปแทน

คลิกที่ปุ่ม "Add to Chart"

อินดิเคเตอร์จะถูกเพิ่มลงในกราฟของคุณโดยอัตโนมัติ คุณสามารถคลิกที่รูปฟันเฟืองข้างชื่ออินดิเคเตอร์บนกราฟเพื่อเข้าถึงหน้าต่างการตั้งค่าและปรับแต่งตามความต้องการของคุณได้